As interest rates have risen over the past two years on the back of rising inflation, Pakistani banks have seen a significant increase in their net interest margin – the difference between the average interest rates they charge borrowers and the average interest rate they pay out to depositors – which has flowed through to the banks’ bottom lines, resulting in rising profitability despite a slowdown in loan growth.

“Improved earnings visibility on [net interest margin] NIM expansion and so far a benign asset quality environment, has driven the strong valuation re-rating, in our view,” wrote Murad Ansari, a research analyst at EFG Hermes, an investment bank, in a note issued to clients on January 23, 2020.

“We recommend sector exposure as the earnings recovery should strengthen, uplifting 2020e ROEs to 16%. Pakistani banks’ valuations remain attractive at 7.0x estimated 2020 price-to-earnings ratio and 1.0x price-to-book ratio. Excluding National Bank of Pakistan, those numbers are a price-to-earnings ratio of 8.2x and a price-to-book ratio of 1.4x.”

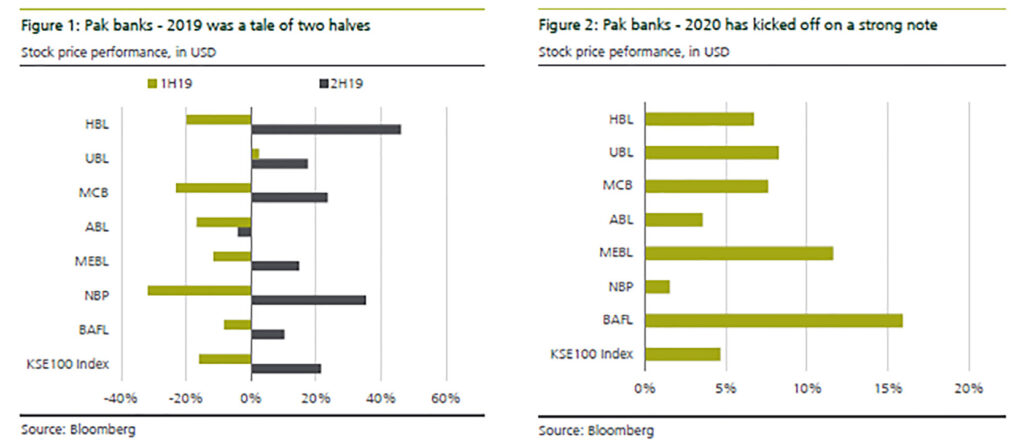

As EFG Hermes notes in its report, the year 2019 seemed to be the harbinger of a recovery in banking sector profitability: after a painful first half of the year, during which stock prices for the entire banking sector fell substantially, at least in US dollar terms, prices have since stabilised and recovered during the second half of 2019 and appear set to continue their recovery well into 2020.

“After a poor first half of 2019 performance (-16% total returns on the sector’s stocks in US dollar terms) driven by strong macro adjustments, our Pakistan banks coverage rebounded strongly in the second half of 2019, rising 22% on average in US dollar terms. This momentum has continued into 2020 with our coverage rising 7.9% year-to-date (up to January 21),” wrote Ansari.

Nonetheless, the picture is not all rosy: net interest margins have improved, but there remains a general stickiness to lending rates that the banks have not been able to match on the rates paid out to depositors, especially those who have savings accounts – which account for approximately 40% of all bank deposits – since those accounts have interest rates regulated directly by the State Bank of Pakistan (SBP).

“Sector data indicates that loan spreads on the existing balance sheet rose 83 basis points between December 2018 and November 2019. This compares to a 325 basis points increase in policy rates over the same period. Rising policy interest rates have meant that funding costs have outpaced asset yield improvement,” wrote Ansari. A basis point refers to one hundredth of one percent.

As the banks’ loan portfolios fully reprice, the net interest margin is set to expand, which forms the basis of EFG Hermes’ thesis for a significant increase in the banking sector’s profitability in 2020.

Rising interest rates on the loan portfolio, however, create two problems for banks: they reduce the demand for new private sector loans, and they increase the risk of defaults on existing loans. While both of these are areas of concern for the banking sector in a rising interest rate environment, there is one major mitigating factor that helps reduce risks in Pakistan: the fact that the government is a dominant borrower and has an almost completely elastic demand for loans.

In effect, the federal government is willing to borrow from the banking sector about as much as they are possibly able and willing to lend. And the government is also – unlike most borrowers – completely insensitive to interest rates.

This is not supposed to be the case: governments are supposed to care as much about their borrowing costs as any other borrower, and Parliament and the public are supposed to hold the government accountable for over-borrowing. However, the government of Pakistan is effectively a heroin addict when it comes to debt and is willing to get more of it at whatever cost necessary.

These are not words that are our opinion or that of analysts at EFG Hermes. They are the opinion of the State Bank of Pakistan, which has said almost as much on several occasions. They do not use the word “heroin”, but they have used the remainder of our description to describe the behaviour of the federal finance ministry when it comes to their borrowing habits.

As a result of the government’s heavy borrowing, particularly after 2008, the banking sector is unlikely to face significant defaults on its aggregate loan portfolio, since private sector lending constitutes an increasingly shrinking portion of their loan books.

The reason why government loans are safe for the banks in a country like Pakistan, which issues its own currency: the government can just print the money to pay back loans denominated in a currency it controls. That action would cause inflation, which would erode the value of the rupee and thus the banks’ profitability in real terms, but it would technically not constitute a default.

However, analysts are still cautious about the extent to which the banks are safe from rising defaults on their lending portfolio.

“The asset quality deterioration has been relatively contained so far, but these are still early days, in our view. We await the release of data from the fourth quarter of 2019 to monitor the banks’ asset quality,” wrote Ansari in his note to clients.

[…] post Rising interest rates fuel stock price rises for Pakistani banks appeared first on Profit by Pakistan […]

Comments are closed.