March 24 should have technically been a good day for the Pakistan Stock Exchange. Right after Pakistan Day, the PSX was finally launching two exchange-traded funds (ETFs), after much hand wringing and regulatory delay for the last four months. Never mind that talks for ETFs had been ongoing since at least 2018.

Instead, on what should have been a good PR day, the launch was converted into a virtual launch. The provincial government of Sindh had imposed a 14-day lockdown on March 22, with a curfew imposed in Karachi from 8pm to 8am, owing to the coronavirus pandemic. The PSX spent that week scrambling to reduce footfall at the office, but also make sure that the exchange could continue to function and – at all costs – stay open.

Farrukh Khan, the CEO of PSX, had been there to witness the mayhem that followed when the exchange closed in 2008. He was determined that under him, the PSX would not repeat the same mistake twice. If the New York Stock Exchange could stay open in the covid-19 pandemic, then there was nothing stopping PSX.

Determined to keep this image of the exchange afloat, he even spoke to Profit for an interview that same week, as if this was a regular PR exercise, as if the very financial world was not on the verge of crumbling in Pakistan.

Though in a sense, if one listens to Khan, it is not. This covid-19 blip will pass, and then the PSX will be forced to reckon with what it has always had to deal with: growing the number of investors, growing the number of listed companies, and nudging the exchange towards international best practises.

Indeed, both the PSX and the capital markets’ regulator – the Securities and Exchanges Commission of Pakistan (SECP) – have continued to work through the pandemic to help make Pakistan’s markets more secure for investors and with a wider, more sophisticated array of products to help incentivise more individuals to utilise the stock market as the vehicle for growing their savings.

The goal appears to be some version of “build it and they will come”, a business aphorism derived from the 1989 movie Field of Dreams. Essentially, the regulator and the market operator are both hoping that if they build a good enough market for investors, eventually Pakistan’s abysmal market participation rates will start rising. It may well be a good strategy, but one that may take some time before it bears fruit.

The scale of the problem

But first, a review of the current situation. Just how bad are market participation levels in Pakistan? Pretty bad, from even a cursory look at the data.

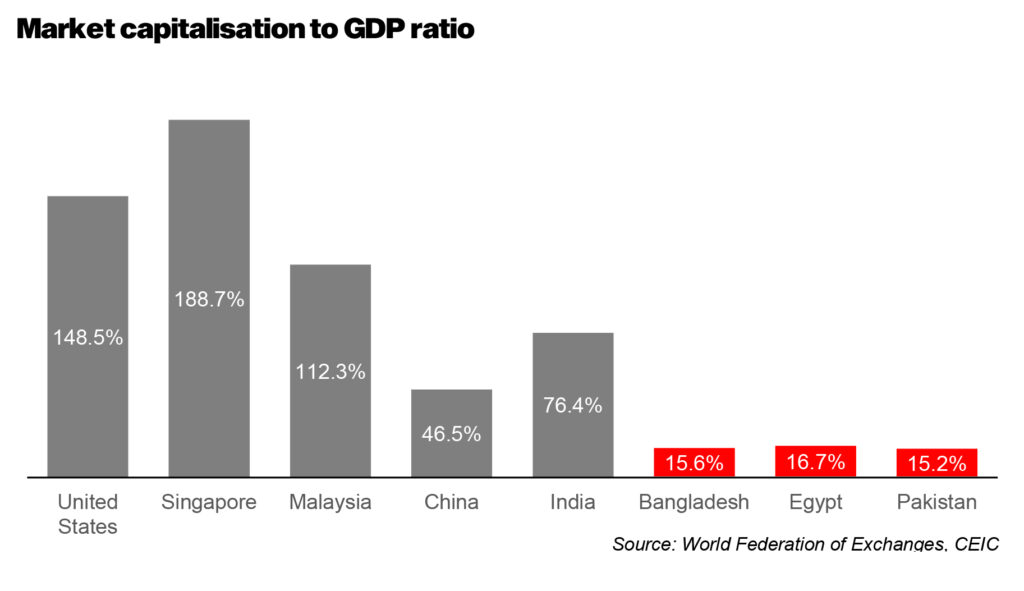

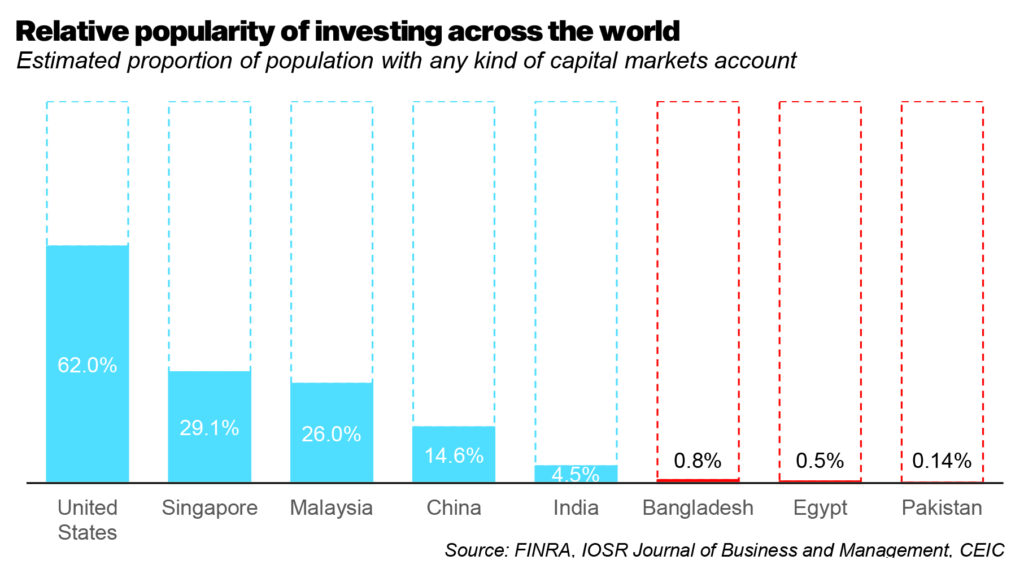

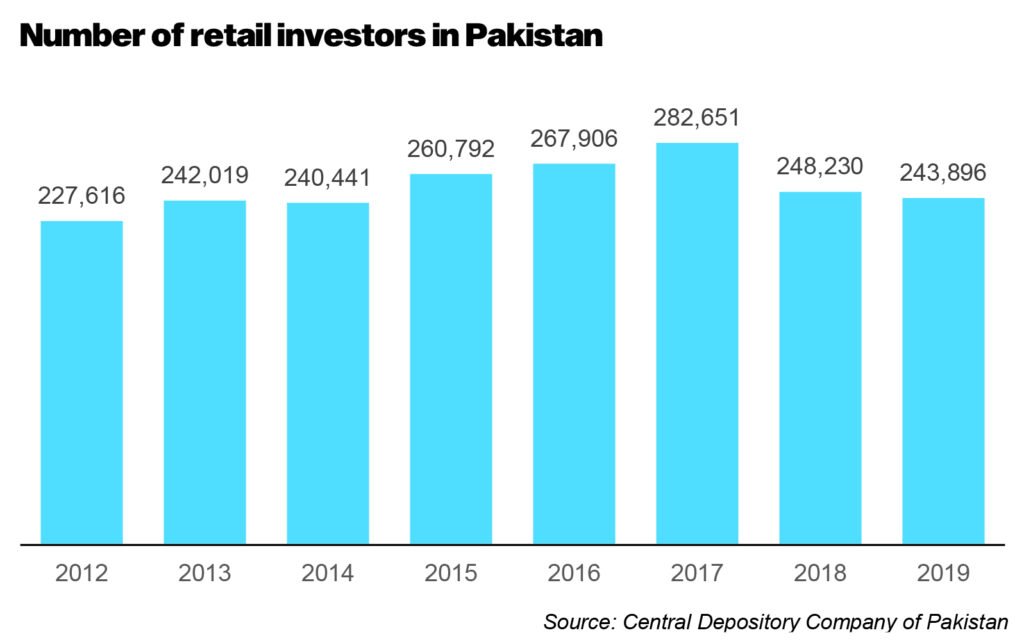

There are just under 244,000 people in Pakistan who have a capital markets account of any kind, according to data from the Central Depository Company (CDC), which amounts to just about 0.11% of the total population. This compares to 0.81% even in comparable economies like Bangladesh. The number for India is 4.5%, and it is a significantly higher 62% in more sophisticated markets like the United States, according to data compiled by Elphinstone, a securities advisory company.

The comparison with Bangladesh is made especially surprising by the fact that the Karachi Stock Exchange, the largest predecessor of the Pakistan Stock Exchange, was founded in 1949, a full five years before the Dhaka Stock Exchange, which was founded in 1954. Incidentally, one of the first listed companies on the exchange, the Karachi Electric Supply Company, is still listed on the PSX as K-Electric.

So why exactly is the situation so bad in Pakistan? Why are Pakistanis so uniquely unwilling to invest in the capital markets?

The reason has absolutely nothing to do with Pakistani stocks as an asset class. Stock market investing in Pakistan – over a long-term horizon – is actually a great investment.

On January 1, 1999, if you had Rs10,000 in your pocket, and you invested that money in a variety of different investment options, here is where it would stand today. To purchase the same amount of goods and services as your could with Rs10,000 in 1999, you would need Rs43,176 today, meaning any investment that you made back then that did not result in you having at least that much money today lost you money.

So here is how the investment options stack up: if you simply bought US dollars with that money, you would have Rs31,827 today. If you bought gold, you would have Rs157,254; if you had bought bonds, you would have Rs75,109. But if you had bought stocks, you would have had Rs355,956. There is, quite simply, no beating the stock market as a venue for investment for ordinary investors.

(Of course, this assumes you had the discipline to stay invested and not try to cash out your money in a panic during the stock market crash of 2008 and the many mini-crashes in the middle. Investing of any kind requires self-discipline.)

So, if it is such a great asset class, why do more people not invest? For that, there are multiple reasons, at least according to the person in charge of running the market.

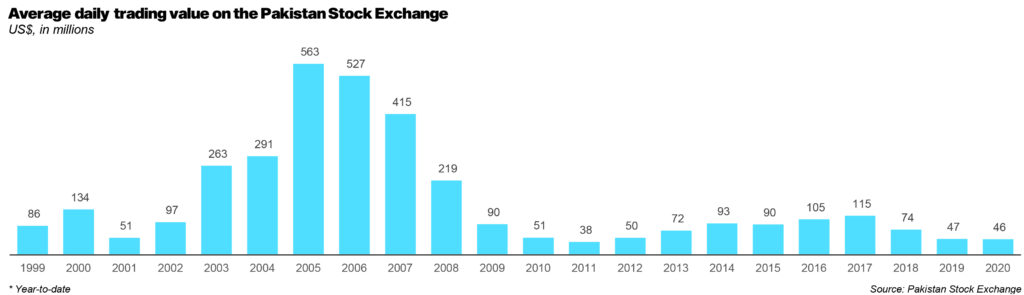

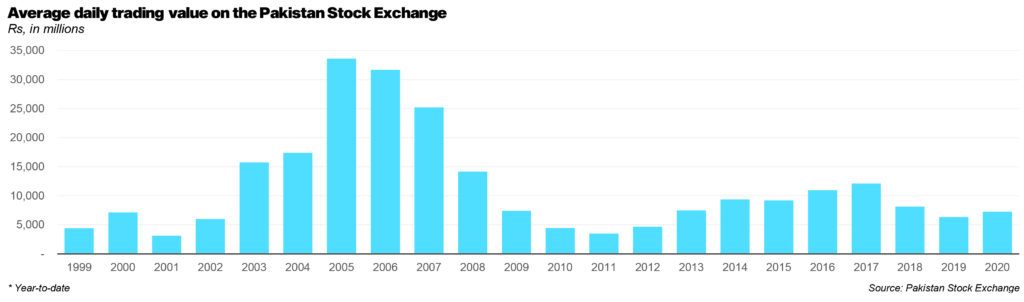

“That’s a loss that really lies with our predecessor, the Karachi Stock Exchange,” said Farrukh Khan, the Pakistan Stock Exchange CEO. “We are certainly [one of] the oldest exchanges in Asia. Many of the other exchanges in Asia were only started in the last two decades. The PSX has not really developed as these other younger exchange exchanges. We’ve had issues with demand and supply, demand meaning the investors and supply meaning the listings.”

Beyond just the supply and demand issues were those of the nature of the exchange itself. “We want to make sure that the credibility of the market is intact, that the demutualization carries on – both here and all over the world. There is also the issue of both a real and perceived conflict of interest. Previously, the brokers who are dealing with the exchange were also owners of the exchange. We are trying to now prove that there is a fair playing field. All exchanges have gone through demutualization and have segregated the brokerage role and exchange ownership.”

But the bigger, more immediate problem, is the fact that Pakistan’s financial services industry – particularly the non-banking financial companies (NBFC) sector – is relatively underdeveloped. “No exchange develops in isolation. Most investors actually come through three industries: pension funds, mutual funds and life insurance. All three industries have not grown in the last few years,” said Farrukh.

“Individual investors – unless they have knowledge or expertise, they will lose money – they often come through these industries. Historically the rules regulating the mutual funds industry were very strict, and only in the 90s and 2000s has it grown. Life insurance – we have some of the largest life insurance companies in Asia, like State Life, but they have not grown in the last decade. There is a growing pension sector, both private, and through the government,” he said.

Given that level of underdevelopment, what exactly does the market and the regulator plan to do to help increase participation from reticent investors? Three things, mainly: better regulations for financial services providers, more streamlined legal requirements for ordinary investors, and more products to invest in.

The SECP’s attempts to help the market develop

For its part, the SECP is working on two fronts. Firstly, it is seeking to create a regulatory regime that allows for a wide range of non-banking financial services companies to exist in the market and offer a variety of services to customers in the hopes that they will lead to more people choosing to invest their money in the capital markets. Secondly, it is tightening the regulation around those companies in order to help create more confidence among current and prospective investors that the SECP will crack down on fraud and malfeasance by financial institutions.

Towards the first goal, the SECP has been creating different classes of NBFCs, each of which is regulated under different standards, with varying degrees of scrutiny involved in the granting of licences. In general, the SECP appears to be tightening requirements for licencing, in particular for individuals who interact with the consumer.

For instance, the SECP has created the Institute of Financial Markets of Pakistan (IFMP), which is now responsible for administering licencing exams for all personnel at NBFCs who deal directly with customers so as to ensure that there is a relatively consistent level of professionalism and education among those dispensing investment advice to the public.

IFMP is modeled along the lines of the Financial Institutions Regulatory Authority (FINRA) in the United States, which is charged with the task of administering examinations and professional standards for a wide range of investment professionals in that market.

The latest regulatory changes have come together in a legislative proposal from the SECP called the 2020 Non-Banking Finance Companies and Collective Investment Vehicles Bill, proposed for consideration by Parliament. This bill appears focused largely on granting the SECP more authority to prosecute and punish bad behaviour by financial services companies.

More specifically, it creates severe financial and criminal penalties for operating an NBFC without authorisation from the SECP. Among the penalties created are punishments including “imprisonment of either description which may extend to seven years or fine, which may extend to Rs100 million rupees, or where contravention resulted in substantial loss to other person or resulted in pecuniary gain to the person who committed the offence, to a fine which may extend to Rs100 million or twice the amount of loss caused or gain made whichever is higher or with both”.

But the SECP’s enforcement powers would go beyond just the ability to fine companies for bad behaviour or to seek the imprisonment of executives who are responsible for wrongdoing. The SECP would have clearer powers to shut down entire companies if their behaviour was egregious enough to justify a complete removal of the entire company from the market as a participant.

The goal of both of these changes is to help investors gain more confidence that, while the SECP will not guarantee that their investments will be profitable, it will ensure that they are not defrauded out of their hard-earned money by illicit means deployed by bent investment professionals.

But it is not just about adding regulations. In some cases, the SECP is also relaxing regulations that have been seen by market participants as overly cumbersome, most notably the sign-up process for new clients of brokerage firms and investment banks.

“The challenge, which still remains, is that account opening is cumbersome,” acknowledges Farrukh. “The FATF has some concerns, they have these KYC [know-your-client] requirements. This is rigorous and cumbersome. Then you have to have a specific bank account with a fund requirement.”

He is referring to the Financial Action Task Force, a global intergovernmental body that is assigned the responsibility for cracking down on global money laundering and terrorism financing. Pakistan has been on the grey list of the FATF for the last two years, and has been threatened with being placed on the black list unless financial institutions in the country do more to crack down on money laundering and terrorism financing.

This, of course, makes it difficult for financial institutions to reduce the paperwork requirements for new customers. However, companies are working on the process. “So we are in discussion to make it easier – [the account opening form] is currently 14-15 pages long. The SECP has accepted biometric scanning (to open an account), which they were testing before corona. We are trying to get that in order. So instead of physically opening a brokerage account you can open it online. It’s difficult to give a timeline on this process, it depends on SECP and NADRA [National Database and Registration Authority],” said Farrukh.

New products

Among the biggest developments that has taken place over the past year in Pakistan’s capital markets is the introduction of ETFs being traded on the PSX. Farrukh Khan explained the goal and the implications of having this product available to investors in Pakistan.

“This is the first product in many years for the PSX. And this is a very significant product for the PSX. Globally, there are about 8,000 ETFs with assets under management of $7 trillion. It really is an essential for a stock market, for capital markets to have. There are also many different types of ETFs – fixed income products as well as equity.”

He explained why it had taken quite some time for the PSX to finally launch ETFs, especially since it had first been floated as an idea by the previous PSX CEO, Richard Morin, the Canadian investment professional who became the first non-Pakistani to run the Karachi bourse, which he did during his tenure from January 2018 through May 2019.

“There are various reasons for the delay. The exchange over the last few years has changed quite a bit. It [the Karachi exchange] used to be an exchange that was owned by its members, like other global stock exchanges such as the London Stock Exchange. Then all the exchanges – Karachi, Lahore and Islamabad – were consolidated to make one, more like other Asian stock exchanges. It became a demutualised corporate entity, instead of a mutualised exchange. Then the exchange has a large number of Chinese investors. That’s brought in new products and new innovation, and brought in new trading systems.”

But Farrukh’s approach appears to be better late than never. “We are here now, with our soft launch of the ETFs. We have seen a lot of interest from other asset management companies for more ETFs. I am sure that this will grow as a segment of the capital market, since it combines tradability of an investment feature, but also like a mutual fund gives a lot of diversified exposure to the market, and is very easy to buy and sell.”

Keeping the exchange open during the pandemic

A key goal of the current management has been to ensure that people are able to access their stock market investments even during the pandemic, a task easier said than done.

“The PSX has been functioning normally for the last couple of weeks. As soon as I joined, I spent a lot of time in anticipation of this virus deteriorating. We used to have a footfall of 200 people in the exchange office. But since the lockdown, we’ve gotten most people working from home. No one can tell from the outside,” said Farrukh, with a laugh.

“There were some technical issues when the lock down was announced,” he said. “We needed to make instant recoveries. We also had to coordinate with exchange and brokers, to have fewer footfall in the market. For the PSX to work and function properly, you need about 200 people. We brought that down to 20 people, which is the kind of footfall reduction you need. Because of the virus, and its socialised aspect, it is critical to take care of employees. We also had to manage the technical and functional challenges, for our companies, for brokers, for investors.”

Farrukh’s experiences from 2008 taught him that keeping the exchange open so that people could continue to access their money would be a crucial task for the PSX management during the pandemic. “It’s not just the banks that are open, the PSX is an essential service. Every country’s exchanges are working, there’s no reason for us to be an exception. We closed the market in 2008, and that was a disastrous step, which hurt the confidence of the market. We haven’t fully recovered from that disaster.”

“In 2008 I was a member of the exchange and when the meeting was held [about whether it should be shut] I was one of the few who said no. Now people tell me they wished they had listened to me,” he said.

I think people are slowly beginning to notice the changes in the markets but instead of focusing only on equity, we should also focus on other areas like Real Estate, Forex, Stocks, Bonds, etc. I’ve been doing a lot of research and believe that investing in Real Estate would give us the best return on investment. Demand in low and supply is high. Buy low now and sell high later but back to your point, will investors notice and which community will offer the best ROI. Please share your thoughts

Can you please tell what percentage of woman are participating in psx ???

Comments are closed.